SUPERCOM Interesting stock. Elements of a turnaround in the framework of a startup. It is back where it was six years ago, after a huge fall and more than five years of going nowhere.

Nasdaq: SPBC. PE 10.31

Note the interviewer is Lazarus InvestmentsPartners, an Investor in Supercom

Introduction(LAZARUS) . Every once in a while we walk out of a first meeting with a management team and are interested in immediately buying stock in the company they run. That was the feeling we had the first time we met with the team from SuperCom (SPCB). We were so intrigued by our initial visit that we followed up the next day by returning to their office for a second meeting. Weeks later we became one of the company’s largest shareholders. What we saw, and still see, in SuperCom is the rare combination of:

- a highly incentivized management team with a track record of building shareholder value

- a corporate turnaround to which the market was giving no credit

- an acquisition (now complete) of the company’s largest competitor that nearly triples the revenue base and grows EBITDA 2.5x

- a recurring revenue model with long term visibility

- a loyal customer base that’s extremely sticky

- growth opportunities that offer the prospect of multiplying the top line

- a very low valuation

We’ll give a quick overview of the business but spend most of the article expanding on the above points, followed by an interview with SuperCom executives. (If you want more background on the company, try this article by Tom Shaughnessy, this article by Irit Jakoby, and the company’s recent road show presentation.)

What they do. SuperCom has two business segments which both use proprietary technology to service long term contracts with sticky customers.

The electronic ID [EID] division offers a full solution for managing countries’ digital identity programs, such as drivers’ licenses, passports, and national ID’s. These programs are essential to countries’ operations and also serve as revenue sources for governments. The number of countries with national EID’s is expected to grow by 70% over the 5 years ending 2015.

The RFID (radio frequency ID) division offers complete solutions for monitoring and tracking people and assets. SuperCom focuses on 3 verticals: public safety (offender tracking), home & healthcare (patient and medical equipment tracking), and animal intelligence (herd and pet tracking). SuperCom’s RFID technology has several important advantages over competing products, including battery life that is up to 10 times longer and price points a fraction of competitors’. The slowest annual growth rate among these verticals is 70%, driven in large part by cost savings. One example: the cost for maintaining an inmate for 1 year is $30,000 to $60,000 whereas the annual cost of electronic monitoring is $1,000 to $5,000.

The company sells software, hardware, and services which altogether offer attractive profitability, on an adjusted basis: over 80% gross margins and operating margins over 25%.

Transformative acquisition. Just a few days ago, on December 26th, SuperCom announced that it closed on the acquisition of On Track Innovation’s (OTIV) [“OTI”] Smart ID division. This division is very familiar to SuperCom, since it used to be part of SuperCom before it was sold to On Track. The purchase price to SuperCom was an exceedingly low 3.5x EBITDA.

Before we tell you about the significance of this acquisition let us address a question that is probably on your mind – if the Smart ID division is so attractive, why did OTI sell it, and why did they sell it so cheaply? We met with OTI management earlier this month and they explained that they were going through a restructuring and had to choose which businesses to focus on and which to move out. There was much debate inside OTI, and they considered making the Smart ID business their main focus. In the end though, they decided to sell this segment to their competitor SuperCom and focus on their NFC (near field communication) technology business. SuperCom was the natural buyer because of their prior ownership of this division and because they were its chief competitor. Most other buyers would have had to add significant infrastructure to bring on OTI’s division. The acquisition multiple was so cheap on a pro-forma basis because it’s based on the contribution to SuperCom’s EBITDA; SuperCom already had the experience and the assets so they can just plug and play this division. The multiple would have been higher for another buyer acquiring the division on a standalone basis.

OTI’s Smart ID division was SuperCom’s single largest competitor in the EID business. The two companies were of comparable size and often both made it to the short list on competitive RFP’s. The acquisition positions SuperCom to win more contracts and also reduces the pricing pressure when they bid. It diversifies SuperCom’s revenue base and adds new countries to the client list. This last point is very important since once SuperCom is awarded one contract in a country (eg, voter registration) that gives them a huge advantage when the country wants to add other services (eg, passports and border control) since new services involve only an additional module to SuperCom’s platform, rather than having to install and manage a whole new system.

The financial impact of this acquisition is dramatic. We’ll cover ahead the RFP pipeline that SuperCom is acquiring. On a trailing basis, looking at 2012 pro-forma numbers, the addition of the OTI segment takes SuperCom’s revenues from $8.9 million to $26.3, an increase of 296%, and grows EBITDA to $7.9 million, up from $3.1 million, an increase of 255%. SuperCom’s market cap today is just north of $50 million.

A business Buffett would love. SuperCom’s EID segment has many of the hallmarks of a classic, defensible business – the type Warren Buffett and other savvy investors are drawn to. Globally, there are only about a dozen full service solutions providers for national identity systems. No surprise, governments are very, very picky about whom they entrust to run these sensitive programs. SuperCom has a track record of successfully implementing programs for over 20 governments. If you are a competitor looking to get into this space but haven’t already done it for years someplace else, you don’t have a chance.

The contracts are long term in nature, with stable recurring revenues, often paid monthly. Five to seven years is typical for a contract minimum, as are multi-year renewals. Some of SuperCom’s contracts have been in place for 15 to 20 years. The reason for this is very simple: once you run a massive national program on a system, you can’t switch that easily. Millions of people have ID’s on that system and agencies rely on the system to run their operations, so there are both cost and logistical barriers to switching.

Once you have your technology infrastructure in place with a country, you are a shoe-in for the addition of any new systems the country needs. Competitors will offer entirely new systems and won’t be able to match the price, timing, or convenience that comes with adding an incremental program to a system already familiar and in operation.

Besides impacting national security, SuperCom often services programs that are revenue centers for governments, so contracts tend to grow in size over the years.

To be fair about it, the flip side to having very sticky customers means that the decision-making process for a contract award can take 2 to 3 years. This makes it hard to add new contracts over a short period of time – unless you happened to have acquired a full pipeline of RFP bids, the way SuperCom just did.

The pipeline. In the interview you’ll read SuperCom management get into the details surrounding their pipeline of opportunities. In brief, they are feeling great about things since they not only took out their largest competitor but also got to add that competitor’s pipeline to their own. The combined pipeline included over 50 bids in more than 20 countries. The bids SuperCom has out are at various stages, with a number of contracts expected to be announced in 2014. The contracts vary in size, from $5 million to $150 million. There are larger contracts out there, but SuperCom wisely chooses not to compete against industry giants such as 3M (MMM) and Gemalto (OTCPK:GTOMY).

Based on the interview it sounds like SuperCom only needs to win 10% to 15% of the contracts they are bidding on to keep busy for the next 7 years. Arie, SuperCom’s CEO, commented, “I do believe that, if we can make the most of having both companies combined together, that a win rate of over 10% is very, very achievable.”

What’s possible.

Listen further to what Arie is saying about the magnitude of what’s possible with the EID pipeline of opportunities:

“In the EID market we talk about contracts that, in many cases, can be 3-times larger in size than the combined revenue of SuperCom and OTI. So investors may be surprised to see that — maybe — we’ll announce a contract that will double our revenue in the next three years, just from one contract.”

– Arie Trabelsi, SuperCom’s CEO

After growing revenues from $9 million to $26 million with the OTI acquisition, SuperCom is suggesting that it has multiple opportunities that can again triple revenues to the $78 million range.

Management is targeting growing revenues as much as ten-fold over the next 5 years, to the $200 million to $250 million range-and that’s before accounting for possible acquisitions. Every time we publish an article suggesting that the future of a company might be different from its past we get vitriolic “how dare you!?” comments, and we’re confident this article will be no exception. We do wish to point out that SuperCom was highlighted by Forbes for its 30-fold increase in value this year, so when Arie suggests a mere 10-fold increase in revenues over the next 5 years, it just might be possible.

We’ve chosen to focus on the EID segment more than the RFID segment for this article, but note that management is guiding for RFID contract awards in 2014. This segment is growing even faster than EID and the company feels that their technology is the best on the market, in many instances.

Management also happened to mention a number of sizeable acquisitions that occurred in the RFID space (Safran bought L-1 for over a $1 billion, and 3M bought Attenti for over $200 million, for example), some at high multiples. We certainly see a takeout as a possibility for SuperCom, if not in whole than at least segments of their business.

Management. SuperCom’s management has a long history of turning around companies, growing businesses, and completing accretive acquisitions. As we noted above, this year alone the stock has been a huge winner, yet there’s an ambitious 5-year plan to continue to grow the company to multiples of what it is today. An investment in SuperCom is a chance to ride management’s coattails with their latest venture.

To give you a feeling for how driven Arie Trabelsi is, we’ll point out that to accommodate our schedule, he held the below interview at 1:30 am local time. He hadn’t slept much in recent weeks as he was rushing to get the OTI acquisition financed and closed, but he still made time for the interview. If you are wondering why Arie is so motivated to grow SuperCom, look no further than the Trabelsi family’s 44% stake in the company.

The Trabelsis got involved with SuperCom in late 2010, when the business was plagued with a bloated cost structure and lack of focus under prior management. Note the trend in the company’s operating income, from losses in 2010 to a small profit in 2011 to a handsome one in 2012. Almost as soon as Arie and the new management had the company turned around, they completed the OTI acquisition that tripled revenues. The team has the drive and the record of building shareholder value.

| 2010 |

2011 |

2012 |

| -$1.048 million |

$0.054 million |

$2.006 million |

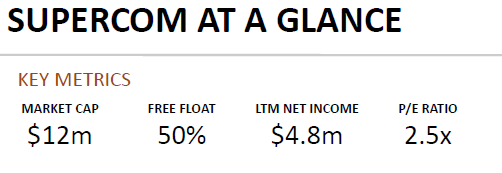

Valuation. Despite the recent acquisition, SuperCom remains under the radar of many investors. And despite the increase in SuperCom’s share price this year, shares remain exceedingly cheap. Simply put, if it’s off the radar today, it was out of the solar system earlier this year. The presentation from just a few months ago showed shares trading at 2.5x earnings. Below is a snippet so you’ll know we don’t make this stuff up.

Shares have increased in price since then, but post the acquisition of OTI, on a pro-forma basis for 2012, we calculate SuperCom’s P/E ratio at the still incredibly low multiple of 6.5x. This number includes some financial income and the adjusted number will look a bit higher depending how you calculate it, but it’s still extremely cheap. It’s worth noting that the company has close to $50 million in net operating losses, so tax favorable treatment of profits is on the horizon.

For the first 6 months of 2013 (SuperCom is an international company that reports differently from US companies), on a combined pro-forma basis SuperCom recorded $0.45 a share in EPS leaving the company at 9.8x earnings from half a year. If second half earnings match the first half, the P/E ratio for 2013 will be 4.9x. Investors buying shares of SuperCom today have a lot of the risks behind them since the turnaround has already proven itself out and the OTI acquisition just closed.

Recurring revenue businesses with highly visible revenues and sticky customers typically trade at high multiples – especially when they have clean balance sheets and minimal warrants and options outstanding, like SuperCom.

SuperCom competes in more than one business and the company’s competitors (see the F-1 for names) are often divisions of larger companies. One competitor, Zetes Industries (BRUSSELS: ZTS) trades at 25x earnings. If we take a discount to that and use 20x, applied to pro-forma combined 2012 earnings, you end up with a market cap of around $170 million, which is more than 3x the current share price.

Recall that this calculation does not include any of the strategic benefits that SuperCom will experience from having acquired its largest competitor. Recall further that there’s a pipeline of over 50 bids outstanding, a number of which they expect to hear back on next year, and at least several of which management took the time to point out could triple company revenues yet again.

If management executes on its 5 year plan and revenues grow to the $250 million range, at a multiple of 2x sales, the stock will be worth over nine times its current price. We believe that 2x sales is the very bottom end of a sales multiple, as some acquisitions have taken place at 6x, so substantially higher prices are possible – but again, it’s contingent on the company growing into something that it is not currently today.

Risks. As stable and as visible as SuperCom’s revenues appear, they are not without risk. This is a technology company, and any failure in the operations or security of SuperCom’s technology could ruffle clients. The company just closed on a major acquisition so the next few quarters will be crucial for management to demonstrate a smooth integration. Contract awards in the industry take years and despite high hopes, there’s no guarantee that SuperCom will win any. SuperCom is based in Israel, so an investment in the company is subject to the risks of investing in that country. The CEO’s family owns a significant stake in the company which may leave some investors feeling they are along for the ride, but we like being aligned with that kind of economic incentive and talent.

Management interview. We offer a very sincere thank you to Arie, SuperCom’s CEO, and Ordan, the company’s Vice President of US Operations. During an exceedingly full month that included financing and closing the OTI acquisition, they made some time to talk to us and summarize the company’s progress and opportunities. We are pleased to share a transcript of the conversation.

Let me kick off by wishing you congratulations on closing the OTI acquisition. Would you tell us a little about the business you just acquired and what attracted you to it?

Arie: Thank you for the congratulations. This acquisition is absolutely transformative for our company. We are all very excited about it. OTI’s Smart ID division was our main competitor in our applicable electronic identity [EID] market because of their size, flexibility, and technological capabilities. This is a very highly synergistic and accretive acquisition for us, both from a strategic and financial point of view. This acquisition means that our largest competitor has joined us to form a very strong solutions provider.

Ordan: Strategically, the acquisition boosts not only our revenues but also our sources of revenues, to different places around the world. We’re expanding to Africa, Asia, South America; areas with great potential going forward and, with the local subsidiaries that provide us with outstanding pre and post sale operations, we can capitalize on that potential to get more and more contracts in those regions of the world.

It also brings in some great employees, very experienced technical and marketing experts in the EID space. People like this are very hard to find because of the high barriers to entry in the EID space – there aren’t many people out there who have this kind of experience.

Arie: Moreover, we are inheriting a huge pipeline of bids around the world and, as some of you might know, the bidding process in the EID space is very long term. It can take two to three years to win a contract. But, once you win these contracts, you have a very long term base of revenues. So we’re inheriting a pipeline with bids in over 20 countries around the world and many of them are close to maturity and we expect to see a number of these awards be given out in 2014, which has potential to increase our revenues significantly going forward.

Lastly, perhaps overlooked by some, a major source of our competitive advantage in the EID space is our technology. The technology we are receiving from OTI is not only complementary to ours, but also consists of a field proven, very robust, and well known platform – Magna. This will help us capitalize on our current strengths to adapt to any customer’s needs around the world, giving us the substantial edge we need to target rapid growth while sustaining a leading position in the EID space.

What are highlights of the financial impact of the acquisition?

Ordan: In terms of revenues, we’re looking at around a near three-fold increase in SuperCom’s revenues on a 2012 pro-forma basis, from around $9 million to $26.3 million.

In terms of margins, in any industry, when you consolidate with a competitor, especially one as significant as this, you can expect a natural margin increase. But here, it’s even more apparent because, besides the overhead costs that are not being transferred over to SuperCom, $5.6M on a 2012 pro-forma basis, there are real operational synergies. Their division is very similar to ours in terms of size, operation, and the nature of the contracts it serves. We have capacity to take their operations and government contracts and place them onto our current division and management structure without having to allocate more overhead costs.

But more than that, as we continue to integrate OTI, we plan to see the same kind of improvements that we saw in SuperCom’s margins over the past three years. As you recall, we’ve done a turnaround on the company that included improving the gross margins and the operating margins. We’ll apply that same process to OTI’s division.

What price did you pay for the OTI acquisition?

Ordan: The price we paid for this division is relatively low for us because its contribution to our 2012 pro-forma EBITDA comes to around 3.5x the price we’re paying. That comes from just the basic overhead cost savings that are not being transferred over to SuperCom. Just removing those overhead costs gives contribution of around $5.6 million.

Arie: I also want to mention R&D. Building the backend technology to serve EID contracts takes a lot of R&D dollars. OTI is coming with terrific technology so we’re going to save more than $5 million worth of net R&D in the next three years just by acquiring this division, and of course also have a more rich and robust software platform, which allows us to bid on many more contracts around the world and hence shorten the time to market and speed up revenue growth.

Taking a step back, would your share some background on the EID industry? What should investors know about this business?

Ordan: The solutions provided in this industry are systems for managing all aspects related to the issuance and usage of a country’s national ID cards, passports, drivers’ licenses, and so forth. They are large, complex systems that are mission critical for the safety and operations of any country, while providing a constant stream of high margin income for the governments.

It’s a very lucrative industry, around $12 billion a year and growing. Most interesting to us is that there are super high barriers to entry. You need to have around up to ten years’ experience deploying these types of systems in other governments before you even bid on an international contract. You can imagine that for systems so important, the governments are very careful who they award them to.

It takes a long time to win a contract in a government, but, once you do that, you enter their infrastructure. You usually deploy a full production line within a government: the printers, the materials, the software, the databases, and the readers. And since it is core to the operations of a government and it takes a while to install it and it also takes a very long and expensive process to remove it, once you are installed in a government, you have very long term recurring revenues. We’ve seen one of our contracts supply us with nearly two decades of growing revenues; it keeps on being renewed.

There are less than a dozen end-to-end turnkey EID solution providers around the world. That makes it sort of a closed group of players with a growing market size so everyone has potential to see some growth, especially the players who are strong in the emerging markets such as SuperCom and OTI’s Smart ID Division which we just acquired.

How would you characterize SuperCom’s track record in the industry?

Arie: We at SuperCom have an impeccable record that every one of our systems that has been installed and delivered has run through for the full length of the contract, something which can’t necessarily be said by all the players in the industry. And with that capability, you know that your revenues are going to be sticky for a very long period of time.

Also important to mention is that these operations, the electronic ID’s, are actually a source of income for the governments. So, not only are they producing something that’s vital to the operations of the government, but they are revenue generating, making the deterioration of contract revenues even less likely.

Two of our major competitive advantages are our track record and our technology, and both have been emphasized thanks to our acquisition of OTI’s Smart ID Division. Both SuperCom and the Smart ID division have ongoing contracts with happy and satisfied customers, some of them for over 15 years. This gives us strong references to provide to new potential customers. Our proprietary technology offers not only very strong security, but also drives our ability to offer lower prices, shorter deployment times, and very high customization, elements which are of very high importance in the international tenders of our addressable markets.

Between all your contracts, including the newly-acquired ones from OTI, can you mention the names of any countries or agencies that you serve?

Arie: I think that OTI provided to the public some examples — Tanzania in Africa, and Ecuador and Panama in South and Central America. We have contracts in Europe and in Asia.

Separate from the EID business, SuperCom has another business segment that uses RFID technology. Can you tell me about that?

Arie: RFID, we believe is going to be a powerful growth engine for the company for years to come. That’s because we have proprietary products which were developed in the company for many years that have specific advantages over other products in the market, both from a technology point of view and from a cost perspective. Better solutions with easier configuration and with a lower price.

We have a very wide range of products that are proven with thousands of customers in the United States. The next step for us is to focus on the right vertical markets we’ve identified, those that are growing fast and that are large enough to attract attention.

And which markets are those?

Arie: One large one is public safety — think for example of wrist or ankle bracelets that track an individual’s location. 3M has put over $500 million in this market by acquiring companies so they can gain a presence. In this market, our solution is probably the most advanced available. Like in our EID business, in the public safety market once you’ve secure a contract with a government it is likely going to be with you for many, many years with a nice stream of cash or revenue every month. Market research presents that this vertical is growing 200% a year and will be a $6 billion market in 2018.

Healthcare and home care is another vertical. We are providing the IT managers and hospital managers with the ability to track their assets, to track and monitor their patients, to prevent disease, and to make sure that they will be able to comply with regulations, like sanitizing their equipment before it is used by other people. The growth of these markets for electronic monitoring and tracking is about 70%.

The third one is probably the fastest growing one – it’s what we call animal intelligence. We provide solutions that monitor, track, and analyze data from cows and livestock for example, pets as well. A tag on the animal tracks its movement, location, life cycle and, probably most uniquely, you can analyze its health condition to prevent diseases early on. There is a huge return on investment. A farmer can buy our system and get the full recovery of their investment in less than a month.

We are leveraging some key abilities from our EID business – our expertise in database, data analysis and other IT technologies, our proven track record in effective deployment of large decentralized systems, and our experience working with governments and structured bidding processes. This together with our proprietary products’ IP in RFID – the board design, the RF and antenna design, the optimized firmware and the algorithms – gives us a very strong value proposition and competitive offering to secure a leading position in these three verticals.

I’ve seen a bunch of acquisitions in the asset tracking space.

Ordan: Definitely. Some of the companies that we’ve seen, for example, Attenti was acquired for over $230 million in 2010 by 3M. 3M-Attenti is a solutions provider to the public safety market, and is a direct competitor to our public safety solution.

In the healthcare space, a company called AeroScout was acquired in 2012 by Black & Decker for over $240 million. It was acquired at 6x trailing revenues, again representing the rapid growth of this vertical. AeroScout is a solutions provider for the real time hospital market, and is a direct competitor to our healthcare solutions.

For both divisions, meaning both the EID and the RFID segment, it sounds like much of future growth is dependent upon winning new contracts. Would you comment on the pipeline for the next 12 months? If not, specifics, than any commentary that you can share.

Arie: I think the important thing here is that on one side we have contracts which continue to generate revenue on a recurring basis. On the other hand, we have a pipeline of bids in different stages. Some of them are very close to the point of award. Some are in the early stages. Others are in the middle. We believe that, right now, we’re in an excellent position in terms of our pipeline.

In EID, what we have, both from OTI and SuperCom, enables us to potentially see a nice stream of contract awards implemented over the next seven years. We are talking about a wide range of proposals, opportunities or bids that can range from $5 million up to $150 million. When you take them and you put each one on a timeline, you see that you can fill out seven years of revenue just from the award of some of them. If we estimate a win rate of 10% to 15% of those opportunities, I believe we’re going to be in excellent position in comparison to the combined OTI and SuperCom revenue for the year 2012. And I do believe that, if we can make the most of having both companies combined together, that a win rate of over 10% is very, very achievable.

Are you able to provide more specific commentary in terms of how many contracts you have an open bid on? And of those, how many might you hear from back in 2014?

Arie: I don’t know if I can disclose numbers. I could just say that it’s well-known that in the market there are at least, I think, 30 opportunities every year. Now, we don’t bid on all of them because we concentrate on the ones where we have a competitive advantage, for instance with our technology. We have over 50 of open proposals and bids in more than 20 countries and our goal is to secure at least three contracts every year.

Given our uniquely modularized technology solution, securing a contract in a new country is a major goal, because one contract with a country provides us with the ability to get more and more contracts in the same country. Once we get a contract, for example, for passport, we have huge advantage to be awarded other EID contracts. Our technology is deployed in a manner such that we can use the same infrastructure that we built for the passport for all other solutions. This gives us a huge advantage in pricing and time to market. In this situation, governments are not likely to go to a competitor because it’s going to cost them much more money and take so much longer.

Besides hearing back on a number of contracts, what are the other important things that investors should look for out of SuperCom in 2014?

Arie: First of all, I think investors probably will look to see if we are able to integrate this acquisition with OTI. Something very important for us to show to the market is that we’re able to do it and that we have the capability of acquiring companies and delivering synergies.

Aside from integration, which we don’t think will take more than a quarter or two, the big thing is delivering contracts wins. You asked me to talk about things outside of contracts, but there are things about the contracts that I need to explain. Can I promise anything here? Not with certainty. But what is possible is that every few months we could be announcing a new contract award, some of which are very, very large.

In the EID market we talk about contracts that, in many cases, can be 3-times larger in size than the combined revenue of SuperCom and OTI. So investors may be surprised to see that — maybe — we’ll announce a contract that will double our revenue in the next three years, just from one contract.

The other thing our investors should expect to see from us are more and more implementations of our RFID solutions. We are going to bid and secure more and more contracts and deliver more solutions there.

Arie, you have a history of turning around companies, of building and selling companies. What’s the goal with SuperCom? Where do you think it can go over five years? Are you looking to build it up to an exit?

Arie: Our goal is build a strong company with streams of recurring revenue. We would like that our investors will see every year that the number of contracts with recurring revenue is increasing. We are talking long term contracts — five years, seven years — so each new add is cumulative to what we’ve added over the prior few years.

Our goal is to increase our market share to a point that our company will be in the range of $200 million to $250 million of revenue in the next five years. No, that’s not guidance, but I’m telling you what my goal is. And I’m talking about growing organically. I’m not talking about acquisitions on that scale, although we may do some very selectively.

We are not looking to sell the company, although we believe from what we see, more and more, both in the EID market and the RFID markets, that large organizations find those markets very attractive. Given the high barriers to entry, these organizations have made large acquisitions in order to become players in these markets. SuperCom probably can be and will be considered by large organizations as a natural target for acquisition. In terms of increasing shareholder value, though, we think the opportunity over the next few years is much greater when we focus on the growth we can deliver organically rather than seeking or approving an acquisition proposal.

For closing remarks, would you summarize the key reasons why investors should take a look at SuperCom right now?

Ordan: What we’ve done since current management took over is complete a significant turnaround rather quickly. The same type of fast results we achieved at SuperCom, we hope to see with the OTI business we acquired. This capability helps us to grow very quickly in a market where it takes a long time to win contracts. But if you can acquire the contracts as we just did and deploy them on a very lean cost structure, then you’re creating massive shareholder value.

Looking at our peers, our share price may be viewed by some as undervalued. Look at Zetes Industries, ZTS on the Brussels Euronet Exchange; it trades at a P/E of 25. Or consider the L -1 Identity Solutions acquisition at an EV to EBITDA multiple of 20. Some may view our share price as even more undervalued when they add in the Smart ID acquisition at 3.5x EBITDA, and investors may get comfortable with a nice margin of safety when taking into account the recurring revenue businesses model and pipeline of opportunities that could start delivering in the next few months.

Arie: SuperCom is a company that on one hand has very nice recurring revenue — stable, not so sensitive to economic slowdown. And on the other hand, has rapid growth engines that can move the company’s revenue to a very high level. I’m referring to the near-term pipeline in EID and the opportunities we have right now in RFID.

The market likes visible revenues. When investors will look at our company once we’ve seasoned the OTI acquisition, they’ll see our revenue baseline for the next five years, based on announced contract wins. All growth and new contracts will be gravy. Subscription businesses can achieve very high multiples, once people understand them and the steady free cash flows they can generate. A year from now once we will have integrated OTI and hopefully have announced several new contract wins; we could be in a very, very different place.

I mentioned before that my goal is to hit $200 million to $250 million in revenues over the next 5 years, just from organic growth. If we find other acquisitions like OTI where we can add assets that fit into our business very well and where we can pay attractive prices, we’ll consider those opportunities. On 2012 pro-forma we just tripled our revenues, yet I feel that we are only getting started with where SuperCom can go.

Thank you very much, both of you.

48.749535

-123.752662

This signals that Apple is becoming a source of diversification to the broader market, believe it or not, and may even be a source of true alpha generation going into 2014 after a lackluster 2013 with what many agree has resulted in cheap valuations at 12x PE (when the SPX index itself is at 17.5x today). Out of curiosity, I looked into who the smart money institutional owners of Apple are, and I was surprised to find an eclectic collection of well-respected hedge fund managers that are each known for their unique and proven investment strategies.

This signals that Apple is becoming a source of diversification to the broader market, believe it or not, and may even be a source of true alpha generation going into 2014 after a lackluster 2013 with what many agree has resulted in cheap valuations at 12x PE (when the SPX index itself is at 17.5x today). Out of curiosity, I looked into who the smart money institutional owners of Apple are, and I was surprised to find an eclectic collection of well-respected hedge fund managers that are each known for their unique and proven investment strategies.